citiesabc

The State of Real Estate Tokenisation in India

19 Jun 2026

India's real estate sector is not short of superlatives. Valued at over $1 trillion and contributing close to 13% of GDP as of 2025, it is one of the largest and most culturally embedded asset classes in the country.

Yet for most Indians, meaningful participation in commercial real estate — grade-A office parks, logistics hubs, hospitality assets — has remained structurally out of reach. High ticket sizes, illiquid holdings, opaque pricing, and cumbersome title documentation have long been the default experience for all but the wealthiest investors.

Tokenisation, the process of representing ownership or economic rights in a physical asset through blockchain-based digital tokens, has emerged as a potential structural remedy. By converting fractional interests into tradable digital units, it promises to democratise access, improve liquidity, and increase transparency in a market that has historically resisted all three.

The numbers suggest the global appetite is real: the worldwide real estate tokenisation market was valued at approximately $3.73 billion in 2025 and is projected to reach $23.99 billion by 2035, expanding at a compound annual growth rate of around 21%.

India's share of that trajectory is meaningful. The country's overall asset tokenisation market is estimated at $133.5 million in 2026, with real estate expected to account for 31.2% of that total. Institutional investors currently hold a 23.8% share of the domestic market, while retail interest is growing steadily. These are early-stage numbers, but the directional signal is unambiguous.

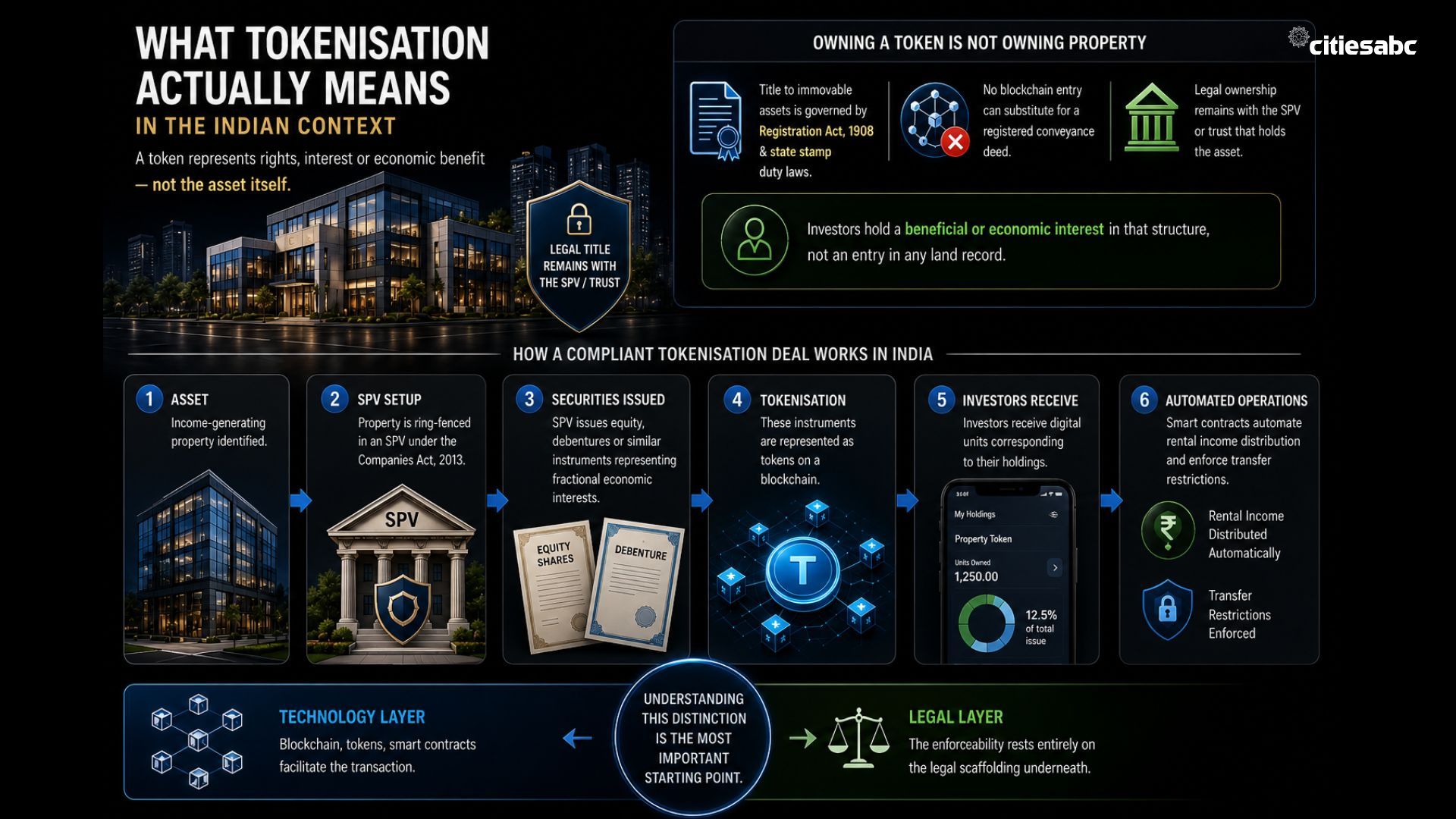

What tokenisation actually means in the Indian context

Before the investment case can be evaluated, the legal mechanics must be understood clearly. In India, as clarified by the proposed Asset Tokenisation (Regulation) Bill, 2026, a token is defined as a representation of "rights, interest, or economic benefit" in an underlying asset — not the asset itself.

This distinction carries enormous practical weight. Owning a token does not mean owning property. Title to immovable assets continues to be governed by the Registration Act, 1908 and state-level stamp duty laws. No blockchain entry can substitute for a registered conveyance deed. The legal ownership of the underlying property remains with the Special Purpose Vehicle (SPV) or trust that holds it; the investor holds a beneficial or economic interest in that structure, not an entry in any land record.

In practice, a compliant tokenisation deal in India looks like this: an income-generating property is ring-fenced into an SPV incorporated under the Companies Act, 2013. That SPV issues equity shares, debentures, or similar instruments representing fractional economic interests. Those instruments are then represented as tokens on a blockchain, and investors receive digital units corresponding to their holdings. Smart contracts automate the distribution of rental income and enforce transfer restrictions. The technology facilitates the transaction — but the enforceability rests entirely on the legal scaffolding underneath it.

Understanding this distinction — between the blockchain layer and the legal layer — is the single most important starting point for any developer, investor, or platform operating in this space.

The regulatory architecture: A multi-regulator maze

India does not have a single statute governing real estate tokenisation. Instead, the activity sits at the intersection of at least four distinct regulatory regimes, each with its own jurisdiction, its own logic, and its own enforcement teeth.

SEBI and the Securities Framework

The Securities and Exchange Board of India is the most consequential regulator for tokenisation platforms. Under the Securities Contracts (Regulation) Act, 1956, any instrument that functions as a share, unit, or marketable entitlement to returns can be treated as a security. SEBI applies a substance-over-form analysis — a principle repeatedly upheld by Indian courts — meaning that labelling a token as "utility-based" or "co-ownership" does not insulate it from securities classification if its economic function involves pooled investment and expected returns.

The most significant recent development in SEBI's regulatory posture is the notification of Small and Medium Real Estate Investment Trusts (SM-REITs) in March 2024, through the SEBI (REIT) (Amendment) Regulations, 2024. These regulations brought fractional ownership platforms (FOPs) — which had been operating in a regulatory grey zone, with estimated assets under management exceeding ₹4,000 crore — under the formal REIT framework. Under the amendment, SM-REITs can pool funds starting from ₹50 crore, issuing units to a minimum of 200 investors, with a minimum unit price of ₹10 lakh. The structure requires an independent trustee, periodic independent valuation, mandatory disclosures, and listed units. It is, in effect, SEBI's answer to the question of how fractional real estate should be regulated: not through bespoke tokenisation law, but by extending the existing business-trust framework.

The CIS Trap: The Elephant Every Token Promoter Must Acknowledge

Section 11AA of the SEBI Act, 1992, defines a Collective Investment Scheme (CIS) as any arrangement where contributions are pooled, returns are expected, assets are managed on behalf of investors, and investors lack day-to-day control. If all four elements are present, registration as a Collective Investment Management Company (CIMC) is mandatory. Operating without it is not merely a compliance gap — it is a criminal offence.

The judicial precedent here is settled and unambiguous. In PGF Ltd. v. Union of India (2013), the Supreme Court held that plantation schemes involving pooled investor funds and promised returns constituted a CIS, regardless of how they were structured or labelled. SEBI's 2008 enforcement action against the Osian's Art Fund established the same principle for art-based pooling schemes. The substance of the arrangement — not its nomenclature — determines regulatory classification.

For token promoters, the practical implication is stark. A fractional real estate token scheme where investor funds pool to buy a property, a platform manages leasing and maintenance, investors receive rental yields and sit passively, will almost certainly be classified as a CIS unless it operates within an SM-REIT, InvIT, or AIF structure. The CIS regime is not a technicality to be engineered around; it is the floor beneath every tokenisation structure.

RBI, FEMA, and the Cross-Border Dimension

The Reserve Bank of India's jurisdiction covers fund flows, foreign exchange settlements, and cross-border investments — all of which are deeply implicated in tokenisation structures that seek to reach NRI or foreign investors. Under the Foreign Exchange Management Act, 1999, foreign investment in Indian real estate is permitted only for specified categories of completed assets. NRI investors can access Indian real estate through NRE or NRO accounts, with distinct repatriation rules: NRE account investments are fully repatriable, while NRO account repatriation is capped at $1 million per financial year. No tokenisation architecture, regardless of how it is structured on-chain, can circumvent these FEMA restrictions.

RERA and Property Law

The Real Estate (Regulation and Development) Act, 2016 governs the underlying asset. A property's RERA registration status is not merely an administrative checkpoint — it is a foundational legal requirement. A tokenisation structure built on a RERA non-compliant property carries those legal defects forward to every token holder. Due diligence on the underlying asset must precede any decision on the tokenisation wrapper.

Taxation: Three Regimes, One Asset

Tax treatment remains one of the least-resolved dimensions of Indian tokenisation. The Finance Act, 2022 introduced a 30% flat tax on Virtual Digital Asset (VDA) transfers with no deductions permitted except the cost of acquisition, alongside a 1% TDS on qualifying transactions. Whether a real estate token is a VDA, a security, or a REIT unit determines which tax regime applies — and each carries materially different consequences. Capital gains on SEBI-classified securities attract a maximum of 20% (with indexation) on long-term holdings. Platform service fees attract 18% GST. Income distributions may be taxed as other-source income. NRI investors must additionally navigate relevant double taxation avoidance agreement provisions. The lack of a clear classification framework creates not just compliance complexity but genuine deal uncertainty at the point of investor evaluation.

The regulated routes of real estate tokenisation in India

Despite the complexity, India does offer clearly defined regulatory pathways for tokenisation. The choice of structure is not optional — it is legally determinative.

SM-REITs: The Fractional Real Estate Route

For income-generating, completed commercial real estate, the SM-REIT framework is the intended pathway. It provides a trust structure with an independent trustee and investment manager, listed units on stock exchanges, mandatory independent valuation, and robust investor protection through disclosure requirements and restrictions on related-party transactions. Tokenisation can sit as a technological layer on top of listed SM-REIT units, but the legal rights of investors flow from the REIT framework, not from the blockchain.

Infrastructure Investment Trusts (InvITs): The Infrastructure Route

Introduced in 2014, InvITs provide the equivalent structure for infrastructure assets — toll roads, power transmission lines, renewable energy projects. Platforms seeking to offer infrastructure yield tokens must operate within this framework. Attempting to market such instruments as unregistered "yield tokens" outside the InvIT structure is precisely the kind of arrangement the CIS regime was designed to capture.

Alternative Investment Funds (AIFs): The Sophisticated Investor Route

For alternative strategies — real estate development funds, art-backed investments, mixed-asset pools — Category II AIFs under SEBI's AIF Regulations, 2012, provide a private placement framework restricted to sophisticated investors. Minimum investment thresholds, placement memoranda disclosure requirements, and prohibition on retail marketing make AIFs the appropriate vehicle for complex or development-stage tokenisation strategies. Tokenisation within an AIF functions as a record-keeping and transfer overlay, not as a substitute for the regulatory framework.

GIFT City: India's tokenisation laboratory

While the mainland regulatory framework is still consolidating, India's most advanced environment for tokenisation experimentation sits within GIFT City in Gandhinagar, Gujarat. The International Financial Services Centres Authority (IFSCA), which regulates all financial activities in GIFT City's International Financial Services Centre, has taken a considerably more proactive stance toward blockchain-based finance than its mainland counterparts.

In February 2025, IFSCA issued a consultation paper on the "Regulatory Approach towards Tokenization of Real-World Assets," covering issuance, custody, trading, clearing, and settlement of digital tokens. The paper called for explicit legal recognition of token rights, defined custody frameworks covering both self-custody and third-party custodians, and stringent AML/KYC protocols calibrated for DLT's cross-border characteristics.

The sandbox approvals granted by IFSCA have produced India's first concrete tokenisation experiments. Terazo, through a maiden $7 million tokenised fund approved under the IFSCA sandbox, became a notable early case study, facilitating qualified investor access to a real estate development project using regulated token mechanics. Realdom India Private Limited's Pinvest Exchange is another sandbox participant, working to establish a platform for fractional ownership of real estate and infrastructure assets.

For platforms targeting institutional or NRI investors from the US, UK, UAE, and Canada, GIFT City currently offers the clearest and most progressive regulatory environment. Entities registered under IFSCA additionally benefit from significant tax advantages: a 10-year income tax holiday on business income within a 15-year window, and zero GST on management fee income.

The GIFT City model is not, however, a workaround for mainland non-compliance. It is a separate jurisdiction with its own rules, and investment by resident Indians through GIFT City structures must be counted within the Liberalised Remittance Scheme's $250,000 annual ceiling.

Key challenges and structural roadblocks

The opportunity is real. The challenges are equally real. For any honest assessment of India's tokenisation landscape, both deserve equal weight.

The Property Law Mismatch

The most fundamental tension in Indian real estate tokenisation is that blockchain operates on a logic of continuous, frictionless transferability, while Indian property law operates on a logic of registered, stamped, and officially recorded transfers. These are not merely procedural differences — they reflect two entirely different theories of how ownership should be evidenced and enforced. Until property law explicitly recognises token transfers as legally equivalent to registered conveyances (which no current legislation proposes to do), the two systems will remain in structural tension. Every transfer of a token representing a beneficial interest in a property currently requires the underlying SPV structure to remain static; it is the SPV that holds the property, and SPV ownership changes may themselves trigger registration and stamp duty obligations depending on the state.

The Secondary Market Gap

Liquidity is the most prominent value proposition of tokenisation. It is also, currently, the proposition least supported by market infrastructure in India. No SEBI-recognised secondary exchange for real estate tokens exists at scale. SM-REIT units are listed on exchanges, but trading volumes for most fractional platforms remain modest. GIFT City's IFSCA is developing frameworks for secondary trading, clearing, and settlement, but these are works in progress rather than operational systems. Platforms that market tokenised real estate as a liquid alternative to direct ownership are, in most cases, overstating current reality. Exit depends on platform-specific mechanisms, counterparty participation, and regulatory permissions — not on the kind of open-market liquidity investors associate with listed securities.

Multi-Regulator Coordination

A tokenisation project that satisfies SEBI's securities requirements can still violate FEMA's capital account rules, RERA's property disclosure obligations, or a state's stamp duty provisions. There is no single regulatory window, no unified clearance process, and no coordinated guidance across SEBI, RBI, RERA, and IFSCA. Each regulator operates within its own mandate, with its own timelines and its own enforcement priorities. For a developer or platform navigating all four simultaneously, the compliance burden is not merely technical — it is a genuine operational and cost challenge that can make or break a project's economics at the structuring stage.

The Smart Contract Risk

Smart contracts govern the distribution of income, the enforcement of transfer restrictions, and the execution of investor rights in tokenised structures. A defective or exploitable smart contract is not merely a technology problem — it is a regulatory and liability problem. SEBI and IFSCA have both signalled that independent smart contract audits from CERT-In empanelled cybersecurity firms are becoming an expected prerequisite for platform authorisation. The cost and timeline of such audits, combined with the requirement to re-audit upon any material contract modification, adds a layer of technical governance overhead that many early-stage platforms underestimate.

Retail Investor Exposure

Perhaps the most consequential risk in the current landscape is the asymmetry of information between token platforms and retail investors. The CIS framework was designed specifically to protect investors who lack the sophistication to evaluate pooled investment schemes. In an environment where some platforms are migrating into SM-REITs, others are operating as private placements to accredited investors, and a third group exists in various states of regulatory ambiguity, a retail investor evaluating token offerings has no reliable way to distinguish between them without significant due diligence. The SM-REIT framework's mandatory disclosures, audit requirements, and exchange listing are precisely the mechanisms that close this information gap — but only for platforms that have formally migrated under it.

The international benchmark

India is not building its tokenisation framework in isolation. The global landscape offers both models to learn from and competitive pressure to keep pace with.

In Singapore, the Monetary Authority of Singapore (MAS) evaluates digital tokens under the Securities and Futures Act framework, applying established capital markets logic to assess whether tokens constitute regulated products. Singapore's approach has produced a well-functioning, internationally recognised environment for security token offerings.

In the UAE, the Dubai Financial Services Authority (DFSA) has established an explicit Investment Token regime, with licensing, AML, and investor protection requirements integrated into a coherent framework. Dubai's ambition to become the tokenisation capital of the Gulf has produced significant institutional activity and attracted global platforms.

In the United States, the SEC applies the Howey Test to determine whether a token constitutes a security — a flexible but judicially tested standard that has produced an extensive body of enforcement precedent. The existence of Regulation D, Regulation A+, and Regulation CF pathways provides structured routes for compliant offerings at various scales.

The EU's MiCA Regulation provides perhaps the most comprehensive harmonised framework, establishing clear categories for crypto-assets, issuer obligations, and trading venue requirements across member states.

India's framework, in its current state, sits behind Singapore and Dubai in terms of regulatory clarity and institutional readiness, though GIFT City's IFSCA is actively closing that gap. The competitive risk is not merely reputational — it is capital. If NRI investors and international institutional allocators perceive greater legal certainty in Dubai or Singapore for India-linked tokenised assets, GIFT City's ability to capture that capital depends directly on how quickly and clearly its framework matures.

The legislative horizon

The most significant signal of India's long-term direction came through the proposed Asset Tokenisation (Regulation) Bill, 2026, introduced as a Private Member's Bill and championed by figures including MP Raghav Chadha. The Bill formally defines tokens as digital representations of rights, interest, or economic benefit in underlying assets, and proposes a regulatory architecture covering the full lifecycle: issuance, custody, trading, and settlement.

While Private Member's Bills face uncertain legislative timelines, the Bill's existence — and the detailed consultation process it reflects — signals genuine policy intent. It positions tokenisation not as a fintech experiment to be contained but as a mainstream financial mechanism to be governed.

The RBI's ongoing Digital Rupee (CBDC) pilot adds another dimension to this trajectory. The e-Rupee's programmability creates the technical foundation for atomic settlement — simultaneous token delivery and payment in a single transaction, eliminating counterparty risk. If the CBDC infrastructure matures alongside tokenisation platforms, it could resolve one of the most significant operational friction points in the current ecosystem.

SEBI's directional posture has also become clearer through its engagement with tokenisation-adjacent questions: its SM-REIT notification, its AIF framework for complex real estate strategies, and its evolving stance on VDA classification all point toward a regulator moving from cautious observation to structured facilitation.

What does it mean for business decision-makers

Real estate tokenisation in India is neither as simple as its proponents suggest nor as prohibitive as its detractors imply. The opportunity is structurally sound: a $1 trillion real estate market, 50 million potential retail investors, world-class digital public infrastructure in Aadhaar and UPI, and a common law judicial system that provides the property rights certainty that institutional capital demands. The cost of building compliant tokenisation infrastructure in India runs 40 to 60% below equivalent projects in Western markets. These are real advantages.

But the current execution environment demands discipline. The CIS trap is not theoretical — SEBI has demonstrated consistent willingness to take enforcement action against unregistered pooled investment schemes, regardless of the technology layer they operate on. The multi-regulator compliance burden is real and requires simultaneous alignment across SEBI, RBI, RERA, and state property law. Secondary market liquidity is nascent, not mature. And the gap between a token's marketing narrative and its actual legal enforceability can be wide in ways that matter enormously when things go wrong.

For developers, the SM-REIT and InvIT pathways offer the most clearly regulated routes to tokenisation at this stage. For institutional investors and fund managers, AIF structures with blockchain-based unit tracking provide both legal standing and technological efficiency. For platforms with cross-border ambitions, GIFT City's IFSCA framework is currently the most enabling environment in India. For NRI investors, understanding the FEMA constraints on repatriation and the applicable asset categories is not optional — it is foundational to evaluating any Indian tokenisation offering.

Technology does not create value. The regulatory structure does not create returns. What creates value is the underlying asset — its location, its lease quality, its income stability, and its management. Tokenisation changes the rails on which that value travels. Building on poor assets or weak legal foundations, with a tokenisation layer on top, produces the same outcome it always has: capital at risk without adequate protection.

India's real estate tokenisation story is being written right now, in SEBI consultation rooms, IFSCA sandbox pilots, and SPV boardrooms across Mumbai, Bengaluru, and Gandhinagar. The companies that will lead it are not those that move fastest. They are those that build most carefully — on regulatory foundations strong enough to support the scale this market eventually demands.

Sources: SEBI (REIT) (Amendment) Regulations, 2024; IFSCA Consultation Paper on Tokenization of Real-World Assets (February 2025); Coherent Market Insights India Asset Tokenization Market Report, 2026; InsightAce Analytic Real Estate Tokenization Market Forecast, 2026–2035; Business Standard; Acuity Law; Mondaq/Beaumont Capital Markets; CoinGeek; Supreme Court of India, PGF Ltd. v. Union of India (2013)